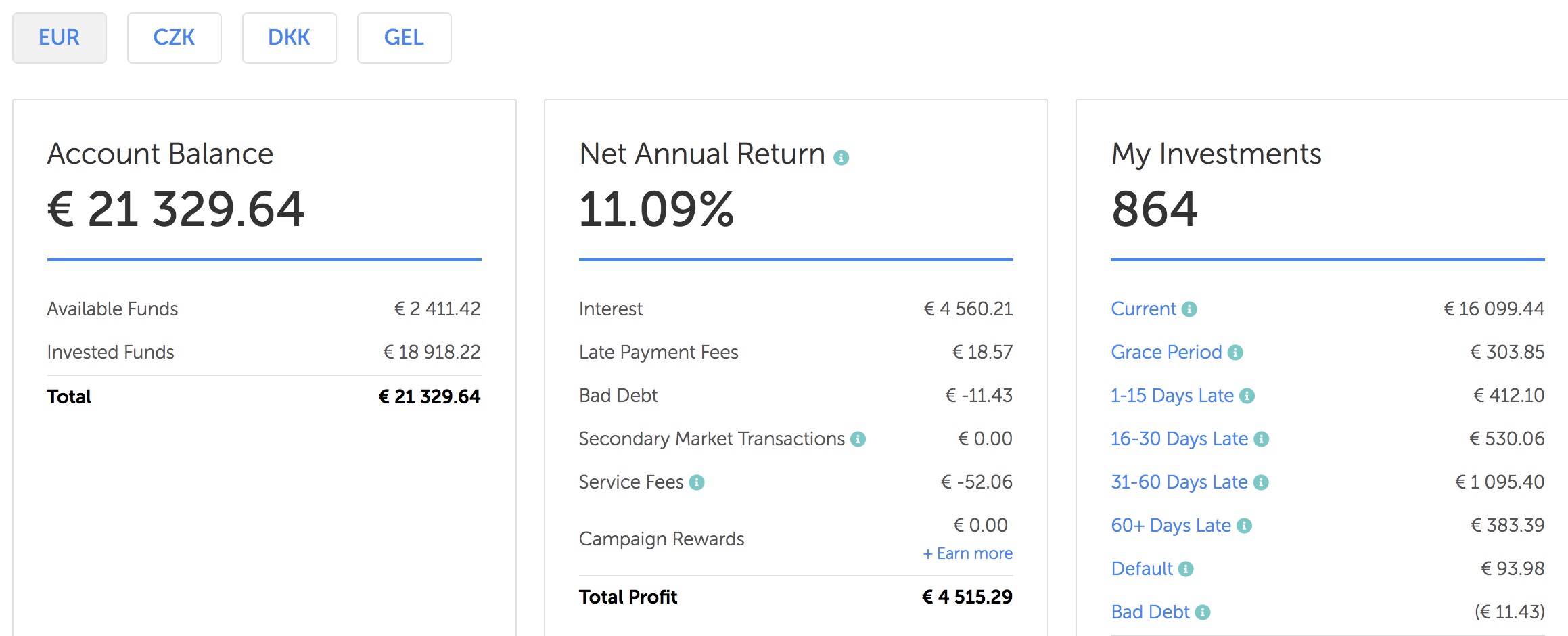

selling bad loans on Bondora secondary market

Last week i have posted all of my defaulted loans on secondary market with a 50% discount. None of them moved out for few days. So i raised the discount to 75% and 78 loans were sold. 85% of them were estonian loans. Only 3 HR Spanish loans. 177 defaulted loans left with total principal … Read more